The past 20 years have seen significant shifts in capital markets. Major trends include interest rates collapsing to zero for a lengthy period and now quickly rebounding. Equity markets shifted meaningfully from active to passive. More recently alternatives have emerged as a sizeable industry with global private capital assets under management hitting $13trn, according to Apollo economics. This still pales in comparison to Global equity markets of $100trn, highlighting the industry potential. One company that’s been at the forefront of this transition is Brookfield Corporation, whose asset management business is the world’s second largest alternatives manager.

CEO Bruce Flatt alongside the management team are by far the largest shareholders and have taken Brookfield from a struggling conglomerate in the 1990s into an investment powerhouse with a value investing framework largely focused on real assets. Flatt, known for his superhuman work ethic and habit of taking the subway to work, has been instrumental in adding new businesses one after another. Brookfield’s success has stemmed from successfully investing its own balance sheet capital and operating its investments. Increasingly they are investing capital on behalf of others within the flourishing asset management business.

Building out the asset management business has been by far the biggest success. The asset management operation despite its large size (managing $450bn of fee bearing capital) has a long growth runway given the industry demand for alternatives and positioning in growth areas of infrastructure and transition strategies. Transition is an innovative strategy to use their vast capital and resources to assist in lowering emissions. In particular, Brookfield sees its Oaktree business taking their credit strategies from $170bn to $500bn over the next 5 years. With the shift from traditional banking to alternative sources of capital Oaktree’s history of strong credit performance sees them well placed for this major industry shift. The regional banking crisis earlier this year in the US will only speed up this trend and opportunity. The traditional banks are in balance sheet repair and conservatism mode due to the impact of higher rates and concerns on their loan books and credit quality. It will be up to non-traditional lenders and the private capital market to pick up the slack.

Flatt and the Brookfield team as long term value investors have made many value creating moves over the years to turn Brookfield into the powerhouse it is today. Over multiple decades, Brookfield’s success has come from investing countercyclically and expanding their investments into fast growing sectors such as renewables and data centres. The ability to invest countercyclically and to take a long-term view is a key strength. Here in Australia, Brookfield acquired Prime Infrastructure post the financial crisis, acquired credit investing powerhouse Oaktree after 10 years of low rates, and the investment and patient 20 year buildout of an asset management franchise are just a few of the many value enhancing moves. In a recent earnings call, Flatt highlighted: “In the decades that we have invested in real estate, we have found that volatile markets often present the best opportunities to acquire high-quality real estate at exceptional values.” Flatt and the team are excited about the prospects for the next opportunistic real estate fund, another example of the value investing mindset.

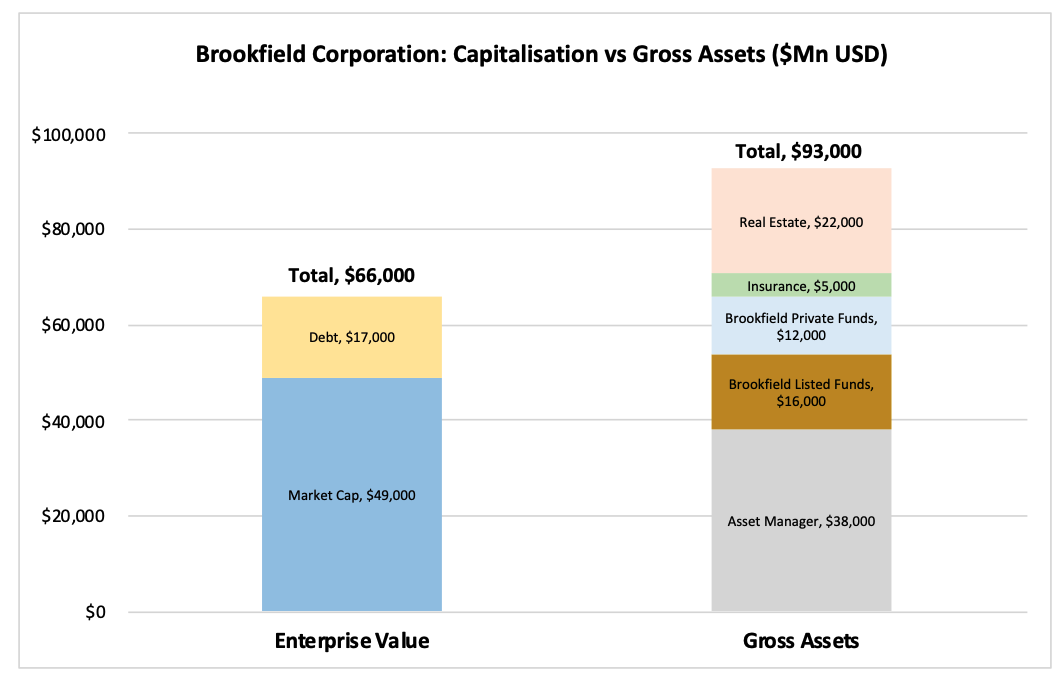

Brookfield financial statements and organisational structures can look incredibly complex, but ultimately, the company is an owner and operator of a range of high-quality businesses and assets. Today several businesses have no ascribed value when compared to Brookfield's USD$50bn market cap. Brookfield has listed vehicles – Brookfield Infrastructure (BIP), Brookfield Renewables (BEP), Brookfield Business (BBU) and Brookfield Asset Management (BAM) that have a combined value at today's market prices of $58bn. This means investors are not paying for Brookfield’s >$20bn of real estate equity. No doubt real estate is coming under pressure, but investors get to own flagship properties such as Manhattan West with 98% occupancy or Ala Moana Centre Honolulu, Hawaii’s premier mall, as upside. These are the types of high-quality properties Brookfield owns on its balance sheet that the market is putting zero value on.

Disclaimer: This material has been prepared by Cooper Investors, published on 5 October 2023. HM1 is not responsible for the content of linked websites or content prepared by third party. The inclusion of these links and third-party content does not in any way imply any form of endorsement by HM1 of the products or services provided by persons or organisations who are responsible for the linked websites and third-party content. This information is for general information only and does not consider the objectives, financial situation or needs of any person. Before making an investment decision, you should read the relevant disclosure document (if appropriate) and seek professional advice to determine whether the investment and information is suitable for you.