Jun Bei Liu, from Tribeca Investment Partners presented A2 Milk at the 2019 Sohn Hearts & Minds Investment Conference. Last year she presented New Oriental Education, which proved to be one of the outstanding picks for HM1, delivering the fund a return of 60% in 4 months. Needless to say, we were excited to have Jun Bei back and have her pitch her latest high conviction idea.

Most people will have seen, heard or tried A2 Milk at some stage. It's in all of our supermarkets and corner stores, and many new mums have given their babies one of the A2 Protein Infant formulas. The difference between A2 milk and regular cows milk is the presence of the A1 protein in regular milk, which may cause adverse digestive symptoms in certain individuals.

The A2 Milk Company is the successor of A2 Corporation Limited, a New Zealand company founded in 2000 by Dr Corran McLachlan, who was researching the health effects of A1 beta-casein, and Howard Paterson, a significant dairy farmer, and a stakeholder in Fonterra, a dairy cooperative. The company commercialised a genetic test to determine whether a cow will produce milk without the A1 protein, and to market A1 protein-free milk.

Ok, so I get that A2 milk is probably healthier than regular milk, but why does Jun Bei think it is such a great investment proposition?

China.

Jun Bei told the audience that A2 is taking advantage of a multi decade thematic to leverage off the world's largest consumer market. With a population of 1.4 billion people, she sees 250 million (10x the entire Australian population) people moving into the upper middle income bracket, with families spending more and more on children's education (New Oriental) and their nutrition.

15 million babies are born in China each year, and the majority of them are fed infant formula from birth to 5 years of age, which is very different to Western culture. Infant formula is a $24b market already, and Jun Bei is seeing an increased shift towards premium brands. The infant formula premium brands have doubled their market share in the past 2 years. A2 is one of the top ten online selling brands in China.

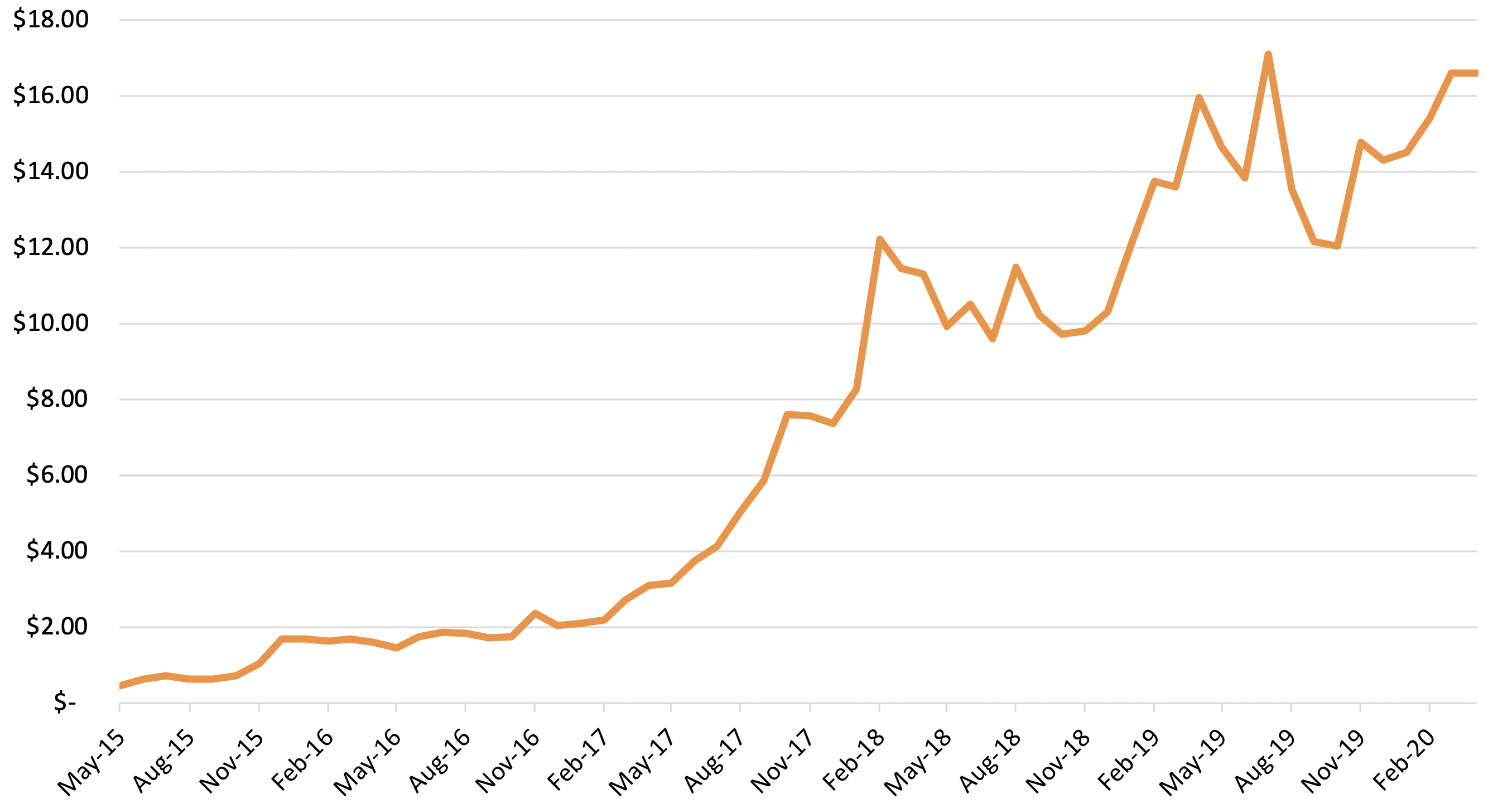

Revenue has grown eleven-fold in the last 5 years, and earnings (based on EBITDA) have grown from $3m to $400m during that same period, and its balance sheet is extremely strong.

Even with recent broker upgrades, she still thinks there is 30% upside to the share price over the next 12 months.

How?

A2 are already doing well in their online business in China, but they are also one of the few Australian companies to have a licence to physically sell their products in Chinese stores. They currently sell in over 16,500 stores across China, and she believes this will grow to over 30,000 stores within 5 years. If A2 can replicate the success of their online business in the physical stores, and the US business continues to grow, she believes that revenue could easily triple again.

She concluded by explaining that while on some of the more traditional metrics A2 may appear expensive, when you price the stock relative to its earnings growth, it remains one of the most attractive investment opportunities in the Australian market.

A2 Milk Company Ltd: Company Details

| Ticker code: |

A2M AU |

| Market Capitalisation: |

$12.3bn |

| Average Daily Volume: |

4.6 million shares / daily |

| 52 week range: |

$11.28 - $17.30 |

| Bloomberg consensus: |

9 Buys, 4 Holds, 42Sells |

| Price target: |

$17.09 |

A2 Milk Company Ltd: Share Price History

Download this stock profile as a PDF.